Conductive Ventures announced it has raised a $100 million venture capital fund to invest in enterprise software and hardware companies.

The fund is led by experienced venture capitalists Carey Lai and Paul Yeh. The fund has already invested in four startups: Ambiq Micro, CSC Generation, Desktop Metal, and Sprinklr. Lai and Yeh first met years ago through a common friend, Kevin Chou, who went on to become founder of Kabam and later KSV Esports. Lai went into venture capital at Institutional Venture Partners and Intel Capital, where he invested in enterprise software companies such as Box and Gigya.

Yeh spent his early career working in product development and hardware at companies such as Ford, Tesla, Next Autoworks, and Fisker Automotive. Most recently, he was a partner at Kleiner Perkins Caufield & Byers. He has worked as a board director/observer with entrepreneurs at AEye, Ambiq Micro, Beyond Meat, Crossbar, Desktop Metal, DJI, Ionic Materials, LuxVue (acquired by Apple), mCube, Motiv, Relayr, and Solidia.

I sat down with them to talk about the fund and their philosophy for investing. The fund isn’t huge, but it will be big enough to provide growth capital to a few enterprise startups per year. It has a relationship with Panasonic in the Japanese market, and the founders take pride in their immigrant heritage.

June 5th: The AI Audit in NYC

Join us next week in NYC to engage with top executive leaders, delving into strategies for auditing AI models to ensure fairness, optimal performance, and ethical compliance across diverse organizations. Secure your attendance for this exclusive invite-only event.

Here’s an edited transcript of our interview.

Above: Conductive Ventures

VentureBeat: When did you get started?

Carey Lai: We launched June of last year. We quickly started making investments. To date we’ve made four investments. We focus purely on enterprise software and hardware. Of the four, we’ve made two software and two hardware investments. I’ll talk about the software ones, because that’s what I cover. Paul covers hardware.

The first one is Sprinklr, which is a social media management platform based out of New York. The second one is called CSC Generation, which is an online consumer leasing platform. They have this vision where anything that can be bought should be able to be leased. They have several direct-to-consumer sites enabling that.

Paul Yeh: A lot of connections from the companies and entrepreneurs carry back before. Same on the hardware side. The first hardware company is Ambiq Micro. It’s an ultra-low-power microprocessor company that supplies to wearables and industrial IOT. It uses one-tenth of the usual battery power. They supply to the Fossil smart watches. With a regular coin cell you can have all the smart functionality and still get a year of battery life without any change in behavior, changing the battery very often, or charging overnight.

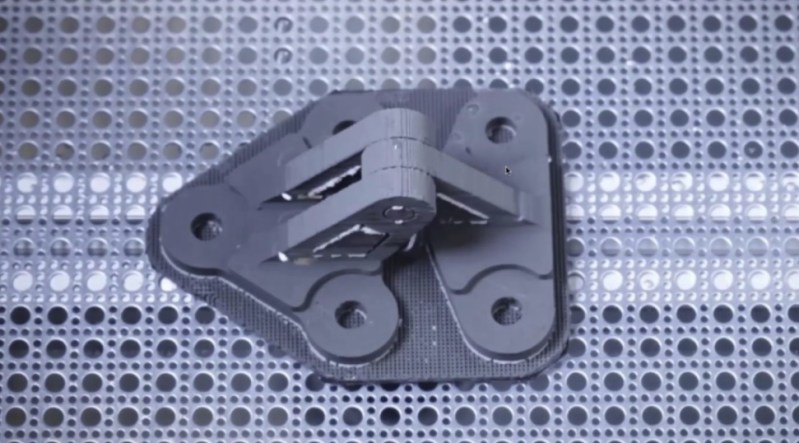

The other hardware company we did is called Desktop Metal. It’s a metal 3D printer company. This is a part that they printed with their machine. It’s a super cool device. The machine is the size of your HP laser printer at work, and instead of printing on paper, it prints layers of metal. You can have very fast prototyping. They’re also building a machine going after the production side. I’ve had a long relationship with the CEO, more than 10 years now. We backed them at Kleiner Perkins, where I came from. When we started this fund we were able to put some money behind them too.

VentureBeat: How much money did you say you have?

Lai: $100 million.

VentureBeat: Enterprise hardware and software is a pretty broad area.

Lai: It is. As we focus on specific on areas, we’re really looking at expansion-stage companies. These are companies that are post-product and have early customer success. Kind of like a series B company. Companies that have anywhere between $1 million and $10 million in revenue would be interesting. Out of that $100 million, we’ll be able to invest in 10 to 15 companies for the total portfolio.

When you look at the number of mega-funds that have been raised — for us, $100 million is plenty in terms of a first-time fund. We’re definitely not first-time investors, but we want to be making these rifle shots into companies that are scaling really quickly.

Yeh: I’d say we’re very picky about the entrepreneurs we back. You know Kevin Chou. He’s an advisor of ours. We were all roommates back in San Francisco 15-plus years ago now. I went to Cal with Kevin. They studied abroad in Hong Kong together.

Lai: The UCs aggregate their education abroad program, UC EAP. That’s where I met Kevin, when we studied abroad for a year. We lived right above each other in the dorms in Hong Kong. We traveled to 15-plus countries together and developed a lifelong friendship.

Funny enough, Paul and I grew up in the same city, in Torrance, California. But we didn’t know each other. It was really Kevin that brought the two of us together. We started our careers in technology investment banking. All three of us were at different banks. Kevin was at Deutsche, Paul was at RBC, and I was at B of A Merrill.

Yeh: We were international even then.

Lai: It was fantastic. Three very young guys learning about finance and technology. To have the three of us evolve our careers over the last 15 years, and then bring it all back together in Conductive, is super fun. We feel very fortunate to be in this position.

Yeh: I still remember the days when — we actually didn’t see each other much on weekdays, because we all came home super late doing investment banking. We’d try to hang out during the day, grabbing lunch together. Kevin would come to my building, grab me, and we’d go to your building to pick you up and walk to Chinatown and have lunch. We hung out late at night when we got home, around 2 a.m.

Lai: Our friendship and a lot of the things we do career-wise are really based on our shared background. All of our parents came here from Taiwan. We all have a similar story of the immigrant path. Our parents came here for a better life, better education. Along with that, they taught us a lot about being frugal, making lemonade out of lemons. No matter what situation you’re in, you have to figure out a way forward.

I think all three of us credit our parents with instilling — we didn’t have a lot growing up, from a material perspective. But what they gave us plenty of was life lessons, values, how to treat others, how to work with other people. Through that foundation and those common values, that enabled our friendship to really grow and blossom.

When I think about the type of entrepreneurs we back, we understand that some of the most prolific entrepreneurs are immigrants or children of immigrants themselves. When I look at Elon Musk or Jerry Yang, or Jen-Hsun Huang at Nvidia, these are all immigrants who’ve built some of the most prolific technology companies in the world. That’s the American dream. In many ways, it’s not about where you come from or your last name or your family history. If you work really hard, if you catch some early breaks, you can, in many ways, build a different inflection point than where you came from.

Yeh: A lot of that is character and grit. Kevin pivoted a few times. There was a lot of never giving up. “This is my shot.” There’s a lot of that grit. I would say the entrepreneurs we back, we look for that character and grit. When we say “frugal,” we mean spending money smartly. You have to be very budget-conscious. That’s something we learned from Warren Buffett. He’s very budget-conscious, and the companies he invests in, right away he’s able to help with operational efficiencies. Again, spending a dollar smartly.

Above: Conductive Ventures

VentureBeat: Did you feel like you brought particular networks into this, in either hardware or software?

Yeh: Absolutely. I started my career in finance, in banking, but after two years I moved to Detroit to work at Ford in product development. I helped launch the Ford Explorer SUV. I also spent half a year in Louisville at an assembly plant. I loved my time at the assembly plant. I’m kind of a geek when it comes to that. I see cars on the road and I tell my wife, “That’s my baby!”

I went to business school at HBS and interned at the McKinsey Automotive Group, as well as Tesla. I really liked my time at Tesla. After school I thought that I was only going to look for jobs at automotive startups. There weren’t many, but I think I talked to all of them at the time. I got a job at a company that was backed by Kleiner Perkins and Google Ventures called Next Autoworks. I was employee 18 or 19, super early. We were trying to sell a fully loaded $10,000 car at Costco. Unfortunately, due to a lot of lobbying and politics from the dealership side, we ended up not raising the DOE loan we needed, and the company went under. But Kleiner pulled me into another company called Fisker. We were trying to do a turnaround there too.

I have lot of automotive and heavy operations background, having worked at factories and covered that whole sector. At Kleiner I helped cover what we called “hard tech,” hardware technology. We looked at robotics companies, self-driving cars, lidar companies, radar companies. We looked at drones. We looked at robots in industrial environments and warehousing, the AGVs or collaborative robotics. We looked at 3D printing because of my manufacturing experience.

I’ve brought a lot of those connections over. I spent close to four years at Kleiner covering all these different things. Coming here, because of our fund size — I know we’re not going to go crazy and write a $50 million check, but my background and connections are enabling me to find things at an earlier stage and very quickly know who to call to validate a company.

Lai: I started my first few years in software investment banking. That’s all I covered, enterprise software. When I got IVP after two years an analyst, what I primarily covered was also enterprise software. This was in the days when it was perpetual license-based and not SAS-based. It was great to experience and invest in that transition, with early companies like Concur, through success factors, and then all the way on to Sprinklr today. It’s been fascinating to see that evolution, not only from horizontal SAS solutions, but also vertical SAS solutions. Being able to do that across the span of 15 years has been fantastic.

Yeh: You actually went across stage at IVP and Intel. You looked at early end growth.

Lai: That’s right. IVP, back in those days, was a much smaller fund. Believe it or not, the fund I started invested out of was a $225 million fund. Their latest fund is $1.5 billion. When I transitioned to Intel Capital, I was investing in –again, this similar stage, what we internally call “early efficient growth.”

VentureBeat: They’ve had some interesting history.

Lai: They have. It’s unfortunate what’s happened.

Yeh: Carey was in the old guard. The investments he did were non-strategic. It’s not like, “Hey, go find semiconductor deals.” What was your mandate? Just go make money?

Lai: Yeah, go make money. I was part of a very small team that focused on internet and digital media. Out of that team, we were investing in things that were completely orthogonal to what Intel was doing. Every other team was dotted-line to a GM. Software and services group was dotted-line to software and services GM. Technology manufacturing was dotted-line to the general manager of TMG. We were the only team that had free rein to do everything else. We didn’t need or have a mandate to do things that were completely strategic.

VentureBeat: Do you guys feel like you have to pay attention to a certain cycle? Is there a cycle that’s good for you right now in enterprise?

Lai: My personal belief is that for VCs, you have to deploy capital. We’d all love to deploy in low cycles. We’d all like to buy homes back in 2009 and 2010. Maybe a little iffy if you’re trying to buy a home now. That’s the same with any kind of investing. It doesn’t matter what the asset is. We’d love to invest when things are low. I also think that the best entrepreneurs are created when times are tough. Only the true crazy entrepreneurs come out when times are tough.

In this current cycle, with this crazy bull cycle we’ve seen, one of the longest in history, I think we’re extremely careful and deliberate with where we deploy capital. We’re very aware of where we’re at in the cycle. We’ve all seen the added public market volatility over last two or three months. We’re not paid to just sit on our hands and not make investments. We don’t have that option. But we’re very aware of — we believe that if you invest in the right companies and the right entrepreneurs, they’ll continue to build value no matter whether it’s an up or down cycle. As long as you’re investing for the long term and building companies of value, that’s what matters.

Yeh: I view it as even more than just the financial cycles. A lot of things cover social and economic impact. Take autonomous driving. You saw the Uber accident in Arizona. Things like that aren’t part of a pure financial cycle. Policy can affect so much of a company’s outcome. That’s important. There’s the Tesla crash, and the whole investigation that came out of that.

A lot of the companies and founders we talk to — the naïve ones think, “All I need to do is build technology and everything else will be fine.” But there are so many other forces at play. It’s not just customer adoption. “I’ll build the coolest tech and people will want to buy it.” Because we invest in enterprise companies, policy and regulation come into play. All of the other AV companies are taking a pause to let Uber and Tesla figure out what’s going on. All of a sudden you have this outside impact, even though it’s not your own company. Waymo stopped their own testing because Uber had an accident. There are lots of things I think about outside of the traditional financial cycles.

VentureBeat: It’s hard to tell what those impacts are going to be.

Yeh: I remember talking to [Joan DeBoer,] the former chief of staff to the secretary of transportation, Secretary [Ray] LaHood. We had a really good chat. She was saying that the prior administration was very good at figuring out how to interact with technology. This one is harder to think about, because there are a lot more labor issues at play.

Bill Ford, we hosted a meeting with him, and he told us that in 17 of 50 states, their number one job is some sort of driver. Truck drivers, parcel delivery, taxis, whatever. When you have technology like autonomous driving, 17 states are going to be heavily disrupted, to the point where you have families out of jobs. The impact of the current climate — how do you think about job displacement? How do you think about how the local and state levels will regulate?

Even with 3D printing, that’s going to be very impactful for operations. But a lot of it, the way we think about it — when you think about a technology like Desktop Metal, how can it help push industry forward? We can help prototype quickly and make better, lighter-weight parts. That’s not going to displace casting and other traditional methods. In a lot of more refined installations, you can have better lattice structures, better weight savings. Overall, if we do this for automotive components, we can have better efficiency, lighter weight, lower costs. But you still have people assembling vehicles. Jobs will still be there. We’re looking at things that could help disrupt industry in the sense that — in my view, it’s still better for society overall.

This company [Desktop Metal] was founded by the former founder of A123 Battery Systems. They’re out of Boston. The cofounders are four MIT professors in materials science and mechanical engineering. This is the printer itself. It prints at normal temperature, but there’s a sintering process that hardens it. You can change the lattice structure so it’s not fully solid. You can have strength without the weight.

Above: Conductive Ventures invested in Desktop Metal.

VentureBeat: Will the pace be just a couple of investments a year?

Lai: Our normal pace would be somewhere between two to four investments per year.

Yeh: But we’ll still look at, on average, about a thousand deals a year. We’re very selective on what we invest in eventually. Right now, the market is really hot, but I would say we can still find the diamonds in the rough.

VentureBeat: Are you focused here in Silicon Valley?

Lai: Primarily here in the U.S. and North America.

Yeh: We’re willing to travel.

Lai: Of the four companies we’ve invested in so far, only one is in San Francisco. The other three are in Austin, Boston, and New York.

VentureBeat: Within software and hardware, is there one trend that gets you most excited? Autonomous driving is a huge one, but on the software side —

Lai: There are many. We’re interested in AI for certain applications, whether that’s AI applied to retail or AI applied to different verticals. That’s very interesting. Horizontal AI probably isn’t as interesting to us. We’re looking at blockchain technologies that are being applied to enterprise. Security, identity, even communications. We’re not interested in cryptocurrency. We’re very interested in vertical software is a whole as well, including SAS 2.0 types of companies.

We span the entire gamut, but again, we’re focused on finding companies that are expansion stage, on the precipice of their inflection point, where we can invest $2-7 million. We’ll definitely lead or follow.

Yeh: I love looking at things in manufacturing — industry 4.0, really. Automation, robotics for factories. Because we’re doing enterprise, a lot of the robots and things you typically see — having lived in a factory, I know the pain points. I’m looking at things like collaborative robotics. When I was working in the assembly plant, we were always told, “keep your head on a swivel.” You never know if a robot arm is about to hit you. The robots are protected in zones, because you can get severely injured. But now I think computer vision technology is there to say, “Are there ways we can work together?” Are there ways we can make manufacturing facilities smaller? We can do 3D printing in a much safer location without a lot of interference. Lots of things in the industry 4.0 space.

Lai: The reason we’re more broad on enterprise software and hardware, which is by no means a small space, is because we’re focused on a stage, the expansion stage. We don’t want to be a niche in a niche. We tend to apply more broadly.

VentureBeat: You guys never got into games, like Kevin did.

Yeh: I still watch and play them.

Lai: He was the one roommate who was literally — I remember him playing Civilization. We’d be coming back home from banking and he’d be playing Civ. I’d just want to sleep for two or three hours before I went back. He’s always been a huge gamer. The stereotyped Asian college guy. Counter-Strike and Doom.

Yeh: I’ve had this talk with a lot of advisors and friends. How do you think about passion versus career? Kevin obviously turned it into a career. I love the physical aspect of making something. I love cars. Is that a hobby, or can I turn that into a career? I followed that path and realized there’s a whole industry with tons of technology behind it. We’re lucky enough to be able to fuse what we really like with our careers.

VentureBeat: I guess you’re not so worried about the big funds, the $100 million —

Yeh: That’s the real growth stage, pre-IPO route. We’re a few zeroes off from there. We’re not competing with them at all. They can write one check bigger than our whole fund. Even if we bought into a portion of something like that, our ownership would be so small it wouldn’t matter. We’re playing in different stages.

Lai: We just like taking this more artisan approach to venture capital.

Yeh: We learned the traditional way.

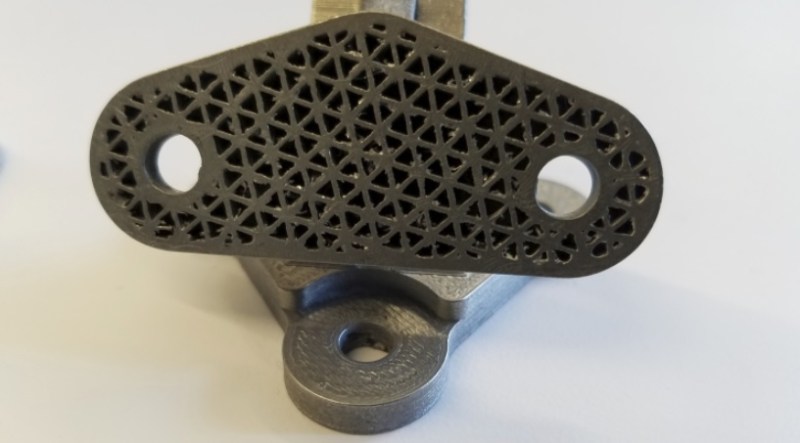

Above: Desktop Metal can 3D-print metal objects.

VentureBeat: That’s not so much the Sand Hill way these days, is it?

Lai: You can do the math. There’s an incentive to raise bigger and bigger funds. The fee income, the scale. We want to be in line with our investors. People say, “Hey, you guys are going to be so successful, you could raise a billion dollars!” I don’t know if it’s that fun, honestly, to have a billion-dollar fund. It’s a lot of pressure, sitting on that much capital and thinking about how to deploy it. We just want to have fun. We’ve both been at big funds, big organizations. At some point it becomes less fun. You have politics.

Yeh: You’re forced to deploy. You can’t just sit on it. The speed increases, and you’re forced to write bigger checks. I used to be fine with a smaller amount, trying to negotiate a better deal, but now five other firms are chasing the same deal, so here’s $200 million for series A.

Lai: A lot of entrepreneurs are often forced to take more capital than they really need. I think about it as — if I said, “Hey, here, eat two years’ worth of food in two months,” you can’t do that. A lot of these companies have a natural digestion path, you know? Inevitably it’s not healthy. For a lot of companies, they either haven’t really figured out product-market fit, or they have an early product-market fit. These investors just pile on a bunch of money.

For entrepreneurs, speed and focus are two things that enable them to be really efficient and really successful. Those are things that big companies don’t usually have. Big companies have resources and capital. They have distribution. They have everything else. A big company can afford to place 100 bets. It’s OK if the majority of them don’t work out. But if a small company starts acting like a big one — “I’ve got this idea, and this other idea, and this other idea” — and you’re funding three things in parallel, it may not be a good idea. A lot of these companies become capital inefficient over time.

We naturally tend to focus on companies that are capital efficient. Maybe in some ways it’s self-selecting. But companies where the entrepreneurs are very deliberate and very focused. They’re thinking about raising $10-15 million, not $100 million. Those are the entrepreneurs we want to back.